Do you currently have a VA mortgage loan? If you wonder whether you qualify to refinance your VA loan with a lower interest rate, the VA Interest Rate Reduction Refinance Loan (IRRRL) could be just the thing you’re looking for.

A VA IRRRL streamline refinance hastens the refinancing process, making it easy to move into a new VA loan product with better terms such as a lower interest rate.

However, it’s important to remember that the VA IRRRL streamline refinance only works for borrowers who currently have a VA mortgage loan. You’ll also need to refinance to a VA loan to take advantage of the IRRRL.

When Is The Right Time To Refinance Your VA Loan?

Deciding when the right time is to refinance your VA home loan requires careful consideration of several factors, including whether or not you can get a better mortgage rate than the one you already have.

While every veteran’s situation is unique and there isn’t a one-size-fits-all solution, there are two popular reasons that borrowers generally consider when determining the ‘right’ time to refinance. These are:

- Reducing the amount of money you pay each month in mortgage payments, and

- Saving on how much money you’ll pay in interest during the lifetime of your mortgage.

A VA IRRRL streamline refinance loan can be a smart choice if you are eligible for a lower interest rate because of the historically low rates in today’s market. This can result in a smaller monthly mortgage payment.

Current Historically Low Rate Environment

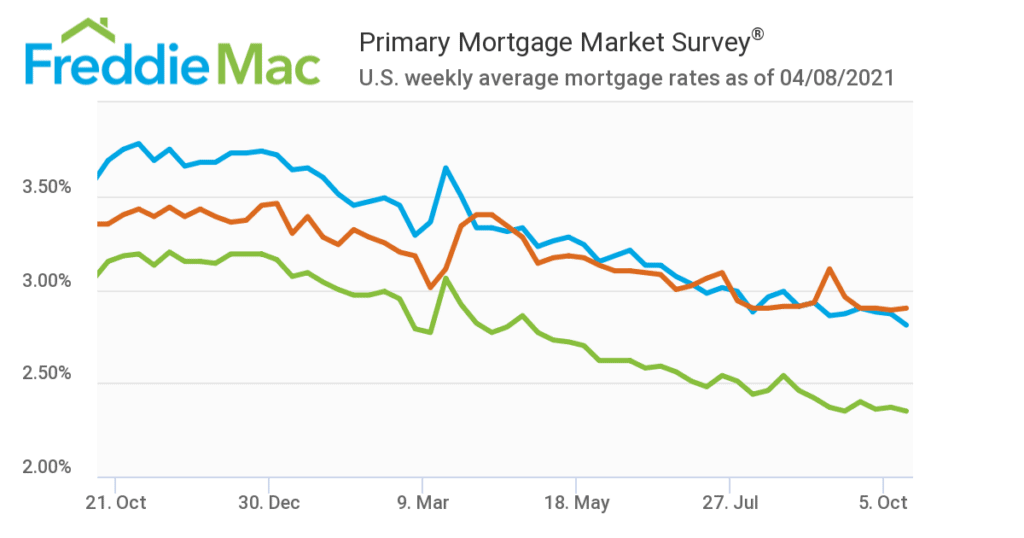

With the current low-interest-rate environment, refinancing a home has never been more affordable. In fact, Freddie Mac recently reported that interest rates are lower than they’ve ever been.

Even saving 0.5% of a percentage point can translate into tens of thousands of dollars over the lifetime of your mortgage.

Step-By-Step Guide To VA IRRRL Streamline Refinance

Because the VA doesn’t directly issue mortgage loans, borrowers will need to reach out to a lender, such as the VA loan specialists at River City Mortgage. Lenders set borrowing criteria, but there is less risk to lenders because the VA backs these loans. That translates into the best possible lending terms for veterans looking to refinance.

While there’s no minimum credit score required for IRRRL eligibility — a VA IRRRL doesn’t require underwriting — borrowers will need to show they have income enough to make the loan payments. These income guidelines, however, are generally more lenient compared to conventional mortgage loans.

Meet Lender Requirements

If you’re interested in finding out more about refinancing your mortgage, you’ll need to reach out to a VA-backed lender. You’ll benefit from connecting with a lender who has a comprehensive understanding of VA loan programs, like the VA loan specialists at River City Mortgage. They’ll not only be able to answer any questions you have about an IRRRL, but they can also speak to the other VA loan programs available and help you decide which is the best solution for your situation.

Because a VA IRRRL refinance loan doesn’t require a home appraisal, you don’t have to spend the extra money or time making that happen. When you obtained your initial mortgage, your home’s value was determined, and that amount will be applied to your refinance. This can be a big relief if your mortgage is currently underwater – if you owe more money than your home’s current assessed market value.

Meet VA Military Service Requirements

As with your original VA loan, you are required to meet military service requirements to be eligible for any benefits administered through the VA. These include the streamline refinance loan program.

In general, however, if you have completed the following, you will be eligible for a VA refinancing loan:

- A minimum of 90 days of active military service during a named conflict

- A minimum of six years of service with the National Reserves or the National Guard, or

- At least 181 consecutive peacetime active duty days

You may also meet eligibility if you are the surviving spouse of a service member who died during active duty or resulting from a service-related disability.

A Certificate of Eligibility (COE) is required, and you can use the COE you initially provided for your original mortgage. If you no longer have your COE, you can apply online through the VA portal to get a new one.

Close Your VA Streamline Refinance Loan

Once you’ve worked through your options with a VA-backed lender and you’ve met the military service eligibility requirements, the only thing left is to complete the closing of your VA IRRRL refinance loan. Closing will be similar to closing on your initial mortgage. You’ll have to sign a few documents and take care of any closing costs you haven’t rolled into the total mortgage amount.

It’s worth noting that the VA IRRRL streamline refinance loan does not have a cash-out offer. You won’t be able to withdraw money from the equity in your home. If this is something you were hoping to look into, the VA loan programs offer a VA CashOut refinancing option. Through the cash out loan program, borrowers can withdraw a portion of the equity they’ve built up in their home. This will lengthen the duration of your mortgage. While it does provide a temporary influx of cash, it may not always be the best solution if your goal is the long-term financial savings typically associated with refinancing at a lower rate or shorter mortgage term.

A VA IRRRL streamline refinance loan can help you lower your monthly mortgage payment, get a lower interest rate, or sometimes both, depending on your situation. To find out how much your new mortgage rates could be, reach out to the regional VA IRRRL specialists at River City Mortgage. We want to help you make your mortgage more affordable and help you put the most money possible back into your wallet.

With home loan interest rates lower than they’ve ever been, it’s a great time to explore refinancing your options and consider switching to a VA IRRRL streamline refinance loan.